#004: On financial planning

Planning our goal pursuit is one of the most laborious things we do on a daily basis, yet it's planning to which we rarely give much conscious attention. How often have you said things like, "I'll do that later, tomorrow or next week" without any real consideration of what "later, tomorrow or next week" already have in store?

In this edition, we will discuss about the important process of financial planning.

A. Financial Planning

Financial planning is the process of estimating financial needs of an individual and to implement a comprehensive plan to meet those financial needs during his or her lifetime through investment. For instance birth of a child, education, purchasing a house, marriage or to meet any emergency expenditure.

Determine Your Current Financial Situation

If you want to plan for the future, you need to understand your current financial position. What are your Incomes, expenses, assets and liabilities/debts? Your net worth is simply assets you own minus liabilities you owe. The net worth is calculated as under:

Your net worth indicates your capacity to achieve financial goals, such as buying a home, paying for university education, future medical expenses etc.

Develop Financial Goals

Your financial goals can range from acquiring assets, saving for emergency as well as investment for your future financial security. The financial goals of an individual can be categorised as below:

Basic financial goals (food, clothing, shelter etc.)

Secondary or advanced financial goals (education, house, marriage, etc.)

Estate planning (Retirement planning)

Individuals can use a variety of investment, risk management, and tax planning strategies to meet their financial goals. These goals change over an individual's lifetime, and accordingly the financial plan should be reviewed on a regular basis for any modifications as per change in circumstances.

TIP: While making financial plans, one should first ensure a planned savings amount and then plan for meeting expenses

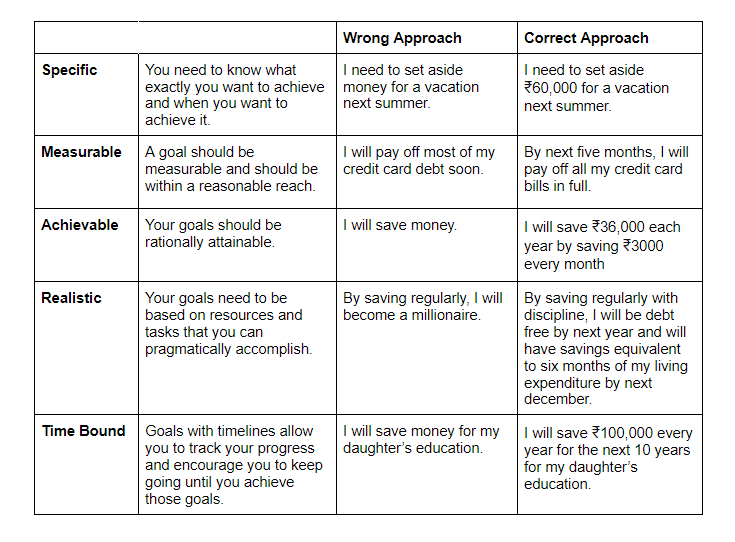

The wealth is not build overnight. One needs to set specific financial goals. A good financial goal should be SMART. Specific, Measurable, Achievable, Realistic and Time-bound.

Goal-based investing focuses on meeting goals that are personal and specific. The focus of this approach is arriving at future value of different goals and then pursuing these goals through asset allocation made for investments for each individual goal. To adopt this strategy when investing, one must plan as per one's age, risk appetite, financial situation and investment horizon.

The Five Step Approach To Financial Goals

STEP 1: Identify specific financial goals

It is important to chalk out a proper plan to earmark each investment with a specific goal. It is important to prioritize goals and aspirations and simultaneously estimate the amount of money it would take to fulfil them.

STEP 2: Classify goals into short-term, medium term or long term

Short-term goals are typically financial requirements that are expected to arise in time period ranging from a few months to one year. Goals like buying a property, starting your own venture, or getting enrolled in a professional course can be medium-term financial goals. Long-term goals may have a time horizon of eight years or more for example planning for retirement course.

STEP 3: Decide upon asset-allocation

Asset-Allocation is a strategy for investing your money into various asset classes such as equity and debt that would suit an investor's income and risk appetite. It is an investment strategy that aims to balance risk and reward - in the form of returns - by dividing a portfolio's assets according to an individual's goals, risk tolerance and investment horizon.

Assets are to be allocated depending upon your age, lifestyle and family commitments and your financial goals. While allocating your funds, it is important to ensure that you distribute your investments across various assets. For instance, in equity, bonds, real estate etc. to benefit from diversification which helps in minimizing risk and enhances the possibility of higher rewards.

Example- 50% in equities, 30% in fixed income bearing instruments like FDs and debt funds and 20% in gold.

STEP 4: Choose the right investments with diversification (within asset classes)

Arriving at the right risk-return combination and choosing the right asset allocation can seem difficult. For a longer term goal, it is advisable to focus on maximizing returns with diversified asset allocation.

Diversification:

In finance, diversification is the process of allocating capital in a way that reduces the exposure to any one particular asset or risk. A common path towards diversification is to reduce risk or volatility by investing in a variety of assets. It aims to maximize return by investing in different assets, investments and areas that would each react differently to the same event, such as those relating to the economy or markets.

Although diversification does not provide guarantee against loss, it is the most important component for reaching long-term financial goals while minimising risk.

-Don't put (invest) all your eggs in one basket (asset class).

-Goal is to find the appropriate balance between risk and return!

STEP 5: Review and revise financial plans

To stay on track, regularly review the progress towards your goals and investments. Review the investments like stocks and mutual funds in your portfolio. Certain products may seem tailor-made for specific needs, but they may not be actually useful for one's portfolio. Be aware of such investment options.

B. Choosing Investment Options & Understanding Risk

This is a crucial aspect in the process of financial planning because an individual is surrounded by abundant choices. Also, every asset class has its own risk and returns. Investments in equities are considered as higher risk investments as their returns are subject to performance of individual companies and general economic scenario. On the other hand, investments in the asset class of debt are considered with relatively low risk. For instance, Government bonds are considered to be effectively "risk free" due to the trust that government will not default on the repayment to investors.

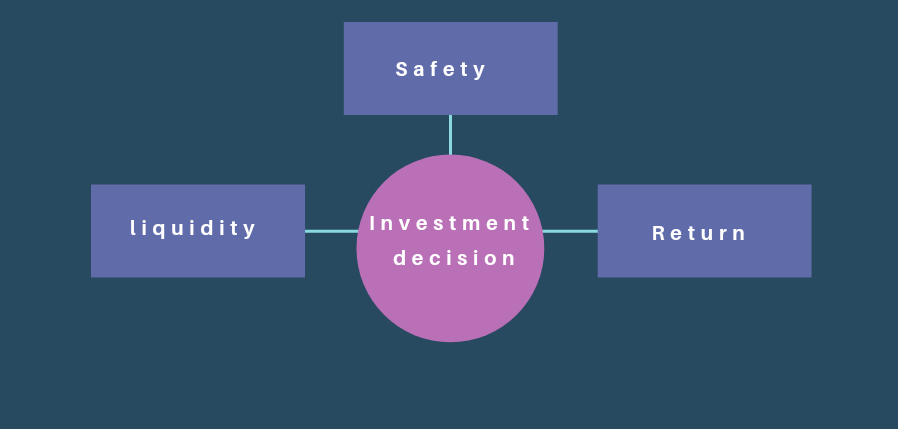

Three pillars of investment: The investment decision by an individual is influenced by safety, liquidity and return.

Safety: This is about how well protected the principal and return of the investment are. For instance, if you lend 100 to someone, will it be repaid on time? Or, is your capital of 100 safe? Safety means your money invested is protected and there is every possibility that on the agreed date, or maybe even before, it would be returned on demand.

Liquidity: This pillar of investment is the degree of ease with which you can encash or liquidate the investment. In the above example, it will be about how soon will you get your money back if you need it immediately?

Return: What is the return you will get on your investments? It could be in the form of income, appreciation of capital invested, or both. Income means an investment's earnings in the form of interest or dividend payment. Capital appreciation means the increase in market value of investment over time. For example, if the present market value is higher than the value at the time of investment, it is called appreciation or gain. In case the market value is lower than the value at the time of investment, it is called depreciation or loss.

C. Returns from Investment

Returns from investment can be described as a gain made by an investor on the investment he or she has made. The returns can be in two forms:

(a) Regular income; (b) Capital appreciation.

Regular Income: This type of return generally comes in the form of dividend/interest received from:

Equity Investment - You get dividends when you buy and hold equity shares of a company and units of equity mutual fund.

Fixed Income Investments - In debt securities, you receive fixed interest on interest bearing Investments.

Capital Appreciation: When the value of initial investment gets enhanced over time and the investor benefits by selling part or whole of the investment at the enhanced value or price.

For example: An investor bought 100 shares of company XYZ Ltd at 50 per share by paying 5,000. When the value of XYZ share increases to 65 per share, and the investor sells 100 shares in the market, he or she will get 6,500 (100 Shares *3 65 per share). The investor stands to gain 1,500 from the initial investment. This is called capital appreciation.

D. What are Risks and Returns?

In financial context, risk can be defined as the probability or likelihood of a loss occurring in relation to your expected returns from any particular investments. It is a measure of the level of uncertainty of achieving the returns as per investor’s expectations.

Risk versus Returns

Risk and investing go hand in hand. Risk has an inherent potential for rewards from investing. It is also well known that higher the risks, higher the associated rewards and vice versa.

Tips:

Once you invest in any asset class you should monitor your investments and keep yourself updated about various market happenings to take corrective action.

Always check the potential risks and do proper due diligence when promised returns are unusually high.

That’s it for today dear reader. See you next week.

Author’s Note:

Hi, if you liked what you read, do subscribe and share with people who can benefit from this. You can also follow us on Twitter/Instagram: @osafarnama and @ashwinkatyal77